Scope emissions explained

What emissions are my company responsible for?

The far-reaching impacts of corporate activity mean that companies influence a wide range of greenhouse gas (GHG) emitting activities across their value chain, many of which are not obviously related to a company’s primary business.

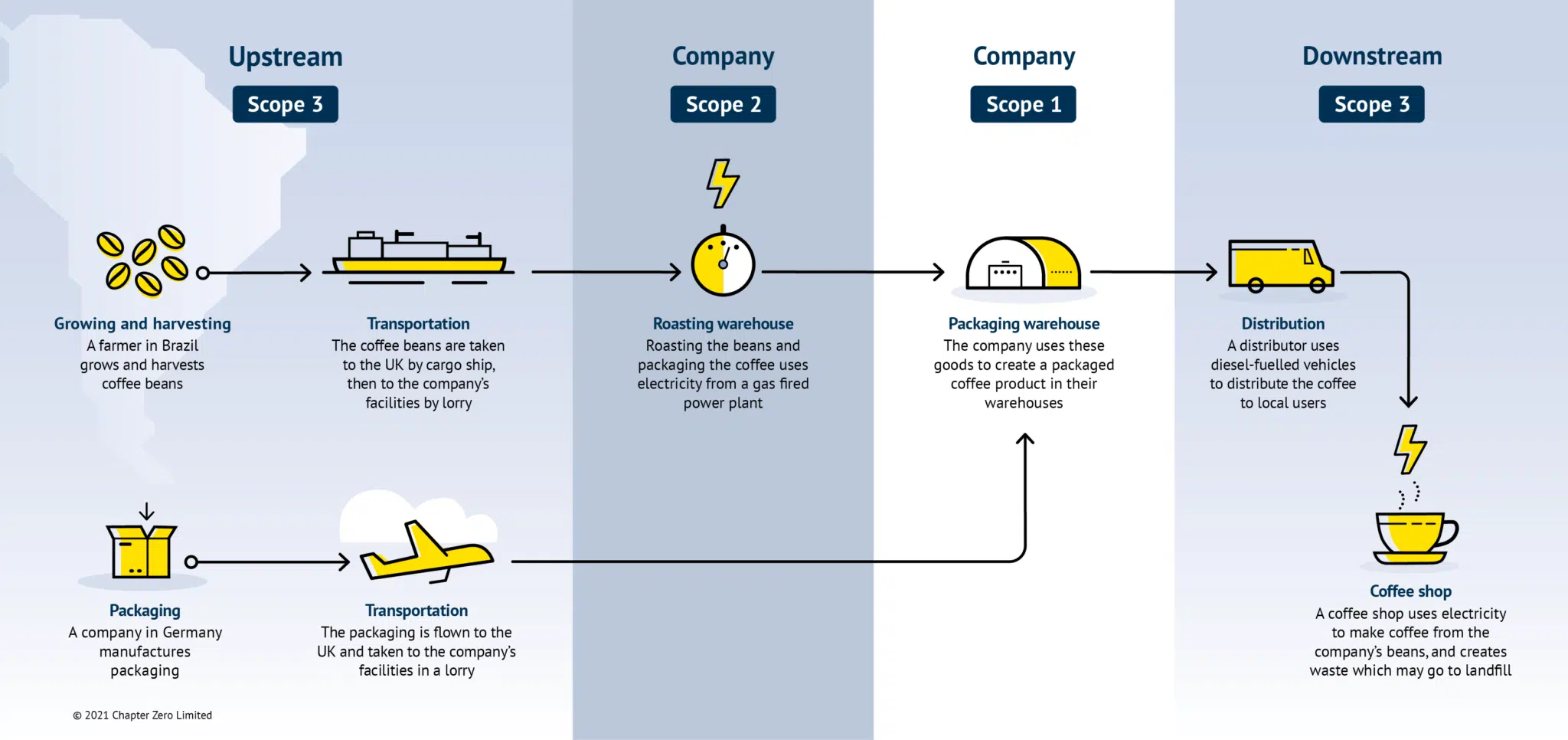

To help companies define the boundaries of the greenhouse gas emissions they are responsible for, the World Resources Institute Greenhouse Gas Protocol has defined three categories: Scope 1, Scope 2, and Scope 3. The GHG Protocol categorises emissions based on how directly they relate to a company’s activities. The Scopes also reflect how much control a company has over certain types of emissions.

| Scope 1

Scope 1 covers direct emissions from sources owned or controlled by the company. This includes emissions from company-owned or operated facilities and vehicles. |

|

| Scope 2

Scope 2 covers emissions from the generation of electricity purchased by the company. |

|

| Scope 3

Scope 3 refers to all other indirect emissions within a company’s value chain. Despite being less directly related to a company’s main activity, these emissions can make up a significant portion of a company’s impact on the climate. Scope 3 can be broadly grouped into two categories: Upstream emissions from activities involved in the creation of a company’s services or goods. This includes emissions from employee travel and commuting to work, and emissions in the supply chain from the production of purchased goods and services the company uses or sells. Downstream emissions occur from the distribution or use of a company’s goods including the disposal of products. If a product indirectly consumes energy during use, for example because it needs to be heated by another appliance, including these emissions in Scope 3 is optional. |

To illustrate these different Scopes, here is an example for a fictional coffee manufacturer:

Understanding and tracking Scope emissions

Related Content

Watch: Taskforce on Nature-related Financial Disclosures

Watch Deloitte's discussion into the TNFD disclosure recommendations, including how they may be used to inform future standard setting and regulations, alongside considering the actions companies can take now to integrate nature and biodiversity into decision-making and reporting.

Audit Committee Dialogue Summary: Transition planning and the changing sustainability reporting landscape

Chapter Zero recently organised a series of two roundtables for Audit Committee Chairs and members in partnership with Accounting for Sustainability (A4S) to explore forward planning, effective communication, and an understanding of emerging requirements for Audit Committees to drive climate action on boards. With expert input from A4S, the second session focused on transition planning and the changing sustainability reporting landscape. These are two topics that are critical for Audit Committees to keep ahead of, and you can find the key takeaways from the second session below.

The TNFD: a briefing to address nature in the boardroom

In September 2023, the Taskforce on Nature-related Financial Disclosures (TNFD) published its final Recommendations for businesses and financial institutions to disclose material interactions with nature. This briefing, produced by the Climate Governance Initiative, explains what these recommendations mean for you as a board director and key questions to ask in the boardroom.