Scope emissions explained

What emissions are my company responsible for?

The far-reaching impacts of corporate activity mean that companies influence a wide range of greenhouse gas (GHG) emitting activities across their value chain, many of which are not obviously related to a company’s primary business.

To help companies define the boundaries of the greenhouse gas emissions they are responsible for, the World Resources Institute Greenhouse Gas Protocol has defined three categories: Scope 1, Scope 2, and Scope 3. The GHG Protocol categorises emissions based on how directly they relate to a company’s activities. The Scopes also reflect how much control a company has over certain types of emissions.

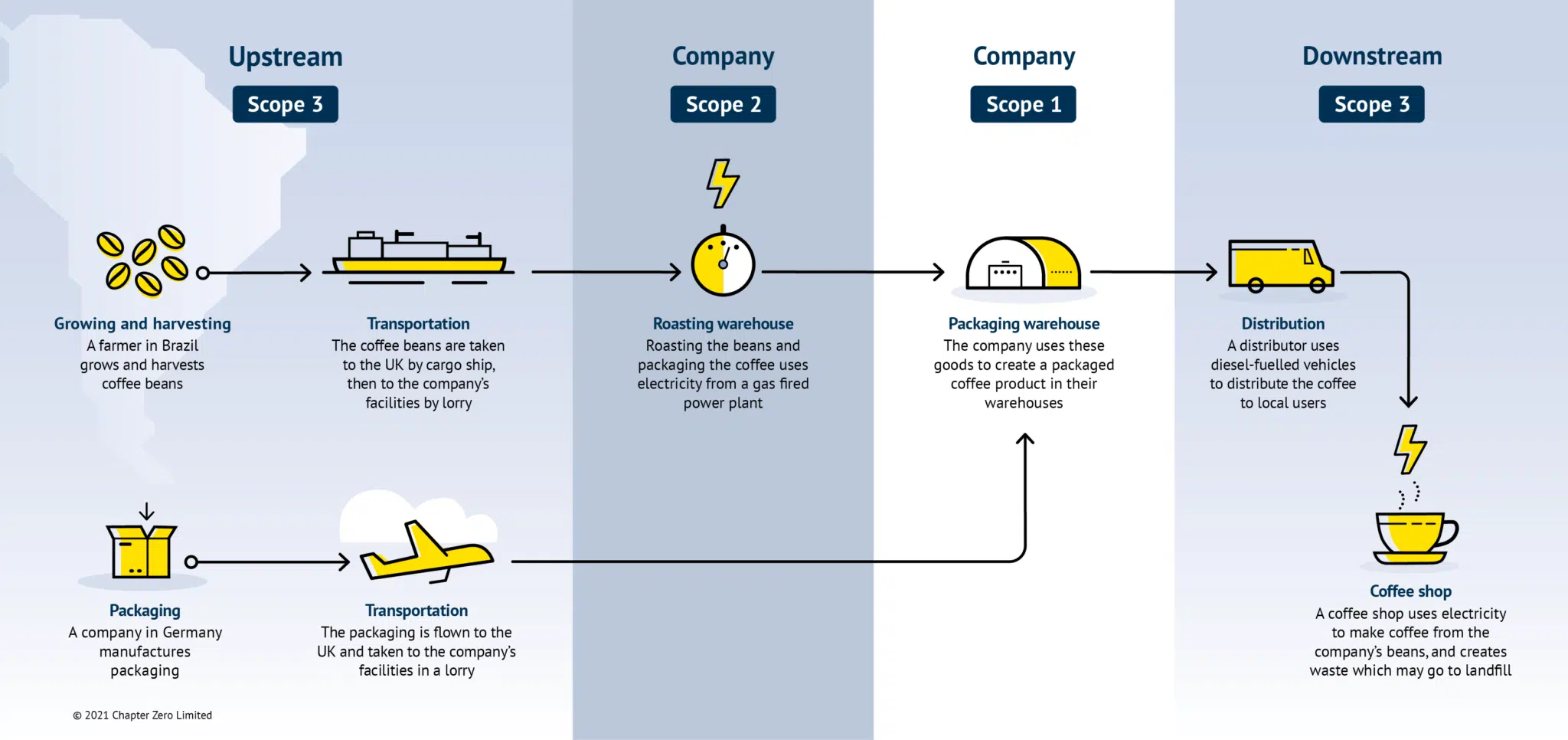

| Scope 1

Scope 1 covers direct emissions from sources owned or controlled by the company. This includes emissions from company-owned or operated facilities and vehicles. |

|

| Scope 2

Scope 2 covers emissions from the generation of electricity purchased by the company. |

|

| Scope 3

Scope 3 refers to all other indirect emissions within a company’s value chain. Despite being less directly related to a company’s main activity, these emissions can make up a significant portion of a company’s impact on the climate. Scope 3 can be broadly grouped into two categories: Upstream emissions from activities involved in the creation of a company’s services or goods. This includes emissions from employee travel and commuting to work, and emissions in the supply chain from the production of purchased goods and services the company uses or sells. Downstream emissions occur from the distribution or use of a company’s goods including the disposal of products. If a product indirectly consumes energy during use, for example because it needs to be heated by another appliance, including these emissions in Scope 3 is optional. |

To illustrate these different Scopes, here is an example for a fictional coffee manufacturer:

Understanding and tracking Scope emissions

Related Content

South Pole 2025 net zero report

Published 10 April 2025, South Pole's net zero 2025 report surveyed 350 financial institutions to better understand how businesses are progressing towards their targets.

Watch: Sustainability Reporting- A perspective from the FCA

Watch this webinar from Chapter Zero and the Deloitte Academy, where we provided an update on sustainability reporting in the UK in March 2025, and the Director of Sustainable Finance at the Financial Conduct Authority shared a perspective on the key focus areas for boards in 2025.